Sustainable Investment Index (SII) Q3: Benchmarking Green Transition Risk in the Capital Markets

Executive Summary: The Financialization of Climate Risk

The Sustainable Investment Index (SII) Q3 report serves as a critical analytical tool, quantifying the financial risk embedded in the climate transition for institutional investors and corporate strategists. This is not an ethical report; it is a risk-management instrument. The Q3 analysis reveals an accelerating divergence in valuations between firms actively managing their carbon transition (low-risk) and those with high structural reliance on carbon-intensive assets (high-risk). The core finding is that green transition risk has become a quantifiable, non-diversifiable factor in the capital markets. This report presents our proprietary Q3 index movements, methodology, and key sectors facing imminent revaluation.

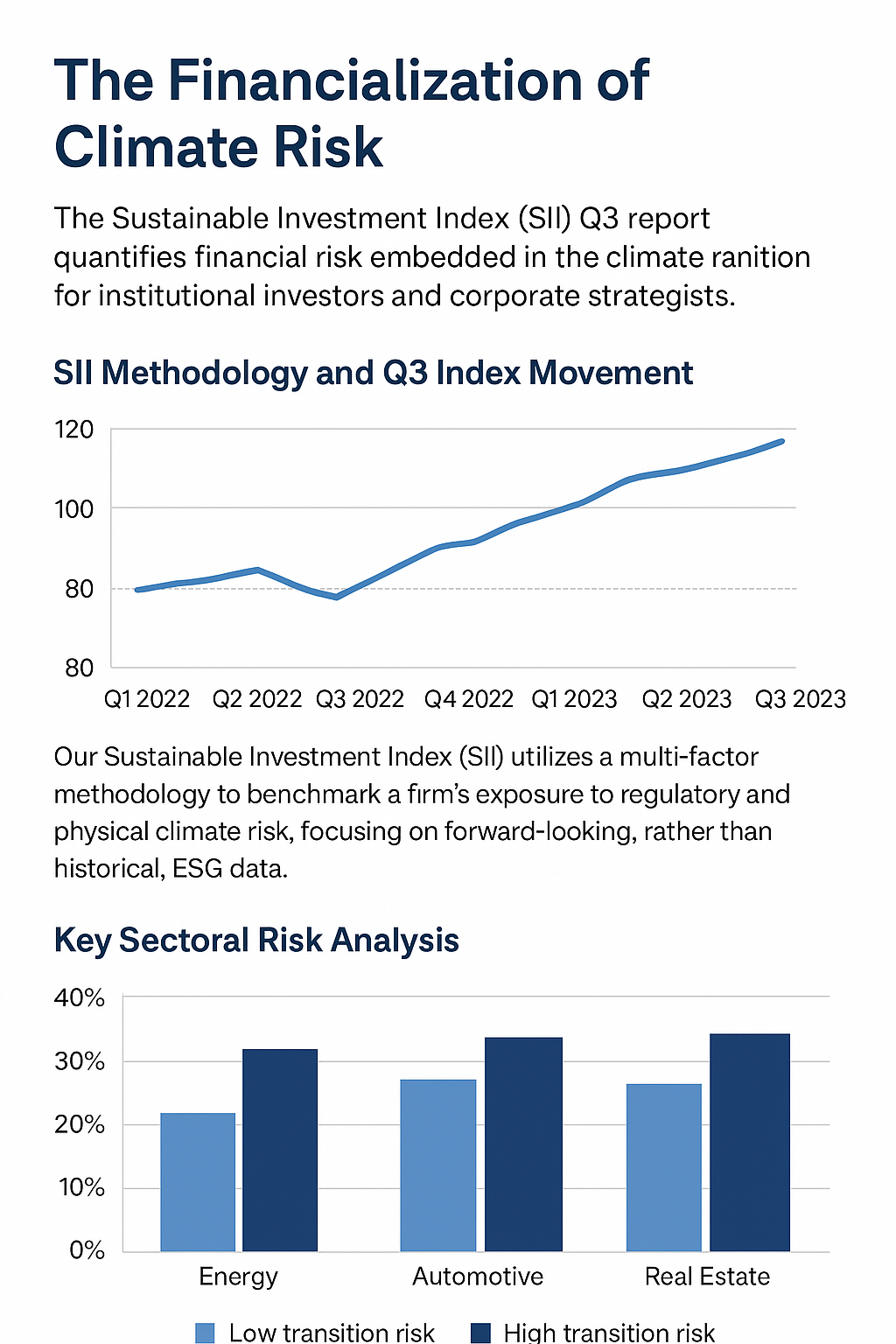

SII Methodology and Q3 Index Movement

Our Sustainable Investment Index (SII) utilizes a multi-factor methodology to benchmark a firm's exposure to regulatory and physical climate risk, focusing on forward-looking, rather than historical, ESG (Environmental, Social, and Governance) data.

- Regulatory Risk Exposure: This factor measures a firm's financial vulnerability to future policy changes, such as carbon border adjustments, mandatory climate disclosures, or increased carbon taxes. Firms with lobbying power often fare better initially, but those with clear decarbonization roadmaps show superior long-term stability.

- Asset Stranding Risk: This quantifies the probability that a firm’s physical assets (e.g., coal plants, long-lived oil and gas infrastructure) will become financially non-viable or "stranded" before the end of their useful life due to technological disruption or regulatory deadlines.

- Capital Reallocation Score: This tracks the firm's expenditure and investment signals, showing the percentage of CapEx being actively shifted toward climate-aligned solutions (e.g., renewables, carbon capture, R&D in green technology).

The Q3 Index Movement showed the largest quarterly spread in history between the top quartile (low transition risk) and the bottom quartile (high transition risk), indicating that the market is beginning to price regulatory and physical climate risk into valuations with high velocity.

Key Sectoral Risk Analysis

The Q3 data highlights specific sectors where transition risk is most pronounced:

- Energy Sector: The divergence between traditional Oil & Gas companies and integrated utility firms is stark. Companies that have successfully spun off or heavily subsidized their renewable energy divisions show lower risk premiums. Investment Mandate: Avoid firms whose long-term financial health relies on 20-year forecasts for thermal coal or unproven carbon capture technologies.

- Automotive and Transportation: The industry faces imminent regulatory change (e.g., end dates for combustion engine sales). The SII benchmarks firms based on the speed of their EV rollout and the rate of depreciation applied to their internal combustion engine (ICE) production assets. Firms moving too slowly risk severe asset stranding.

- Real Estate (Commercial): Commercial property firms show risk based on the Energy Efficiency Score of their holdings. Properties that do not meet anticipated 2030 energy standards are already seeing higher insurance and borrowing costs, signaling a clear risk for long-term holders.

Strategic Takeaways for Asset Managers

The era of soft, non-financial ESG compliance is over. Climate is now a core financial factor.

- Mandatory Transition Audits: Institutional investors must mandate clear, verifiable transition audits from their portfolio companies, demanding data on Scope 1, 2, and 3 emissions and CapEx alignment.

- Active Divestment: The SII strongly suggests that investors actively divest from firms consistently ranking in the bottom quartile of transition readiness, as regulatory and physical risk is highly concentrated and likely to generate significant losses.

- Green Alpha Generation: True alpha in the coming decade will be generated by identifying companies with proprietary low-carbon technologies that can monetize the transition risk of their competitors, providing a defensive hedge against macroeconomic instability.