Public Debt Dynamics: Long-Run Fiscal Stability Analysis for G7 Nations Under High-Interest Scenarios

Executive Summary: The Structural Cost of Capital

The fiscal stability of G7 nations is entering a period of acute, structural stress driven by the persistence of elevated interest rates. This long-run analysis moves beyond annual budget deficits and examines the solvency constraints imposed by the new cost of capital. Our research finds that several major economies now face a critical and rapidly narrowing fiscal window where debt accumulation exceeds GDP growth, forcing imminent, politically costly choices regarding taxation, spending, and central bank independence. This report provides policymakers and sovereign debt investors with the methodology and data to stress-test national balance sheets against persistent high-rate environments.

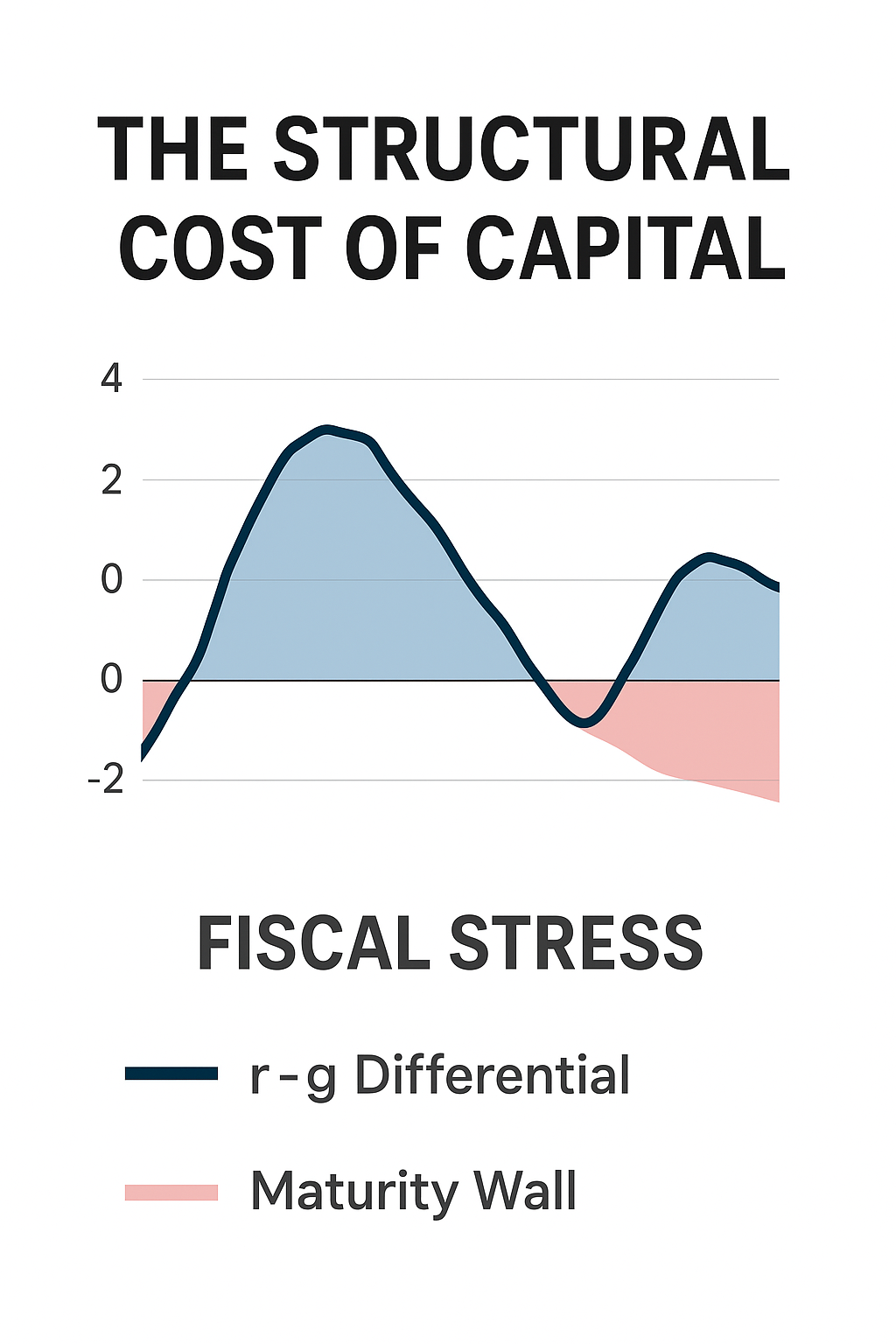

The Critical Solvency Constraint: The r−g Differential

The long-term sustainability of public debt is determined by the relationship between a government's real interest rate on debt (r) and its real GDP growth rate (g). This is known as the r−g differential.

- The Favorable Era (r<g): For decades, growth exceeded the cost of borrowing. In this environment, governments could finance deficits without raising taxes, as economic growth automatically shrank the debt-to-GDP ratio.

- The Stress Scenario (r≈g or r>g): In a high-interest scenario, the cost of servicing existing debt consumes a larger share of public revenue than economic growth can generate. This dynamic is structurally unsustainable and requires the government to run persistent primary budget surpluses (tax revenue exceeding non-interest spending) to maintain a stable debt ratio.

Our analysis of the G7 reveals that the r−g differential has closed dramatically, requiring unprecedented fiscal austerity just to stabilize the debt burden.

Data Spotlight: The Maturity Wall and Fiscal Headwinds

The immediate challenge is the Maturity Wall—the large block of low-coupon pandemic-era debt that is now being rolled over at significantly higher market rates.

- Debt Servicing as a Share of Revenue: Data indicates that interest payments for some G7 nations will soon surpass defense or education spending as the largest non-discretionary budget item. This cost is non-negotiable and crowds out productive public investment.

- The Primary Deficit Problem: Only by running substantial and prolonged primary budget surpluses can nations stabilize their debt-to-GDP ratios under the current r environment. The political feasibility of achieving the necessary surplus levels (often equivalent to several percentage points of GDP) is extremely low, leading to a high probability of fiscal slippage.

- Stress Testing and Solvency: Our model runs a dedicated stress test where the real interest rate (r) is sustained 100 basis points above the real growth rate (g). Under this scenario, we project the mandatory cuts to public spending and the necessary tax increases required to prevent the debt-to-GDP ratio from accelerating past the 150% threshold.

Strategic Mandates for Fiscal Governance

Sovereign debt management must become the central focus of national policy, demanding coordinated action from both the Treasury and the Central Bank.

- Active Debt Management: Governments must prioritize lengthening the average maturity of their outstanding debt. While short-term debt is cheaper, it exposes the national balance sheet to rapid refinancing risk, exacerbating the Maturity Wall problem.

- Institutional Fiscal Rules: Nations should adopt independent, legally binding fiscal rules (e.g., maximum deficit targets or a minimum structural surplus) designed to function automatically under adverse r−g conditions, thereby mitigating the risk of political intervention destabilizing public finances.

- Asset Sales and Revenue Diversification: Governments must urgently inventory and assess the value of non-strategic public assets that can be privatized or monetized to pay down debt without resorting to sharp, growth-killing tax hikes.

In the long run, fiscal stability will not be achieved through wishful growth projections, but through the difficult political decisions required to bring persistent budget deficits into alignment with the new structural reality of the cost of capital.