Global Trade Forecast 2026: Modeling the Future of Supply Chain Resilience and Reshoring

Executive Summary: The Resilience Imperative

The global trading environment through 2026 will be defined by the shift from cost-based optimization to resilience-based diversification. Our proprietary econometric models forecast a structural slowdown in the growth rate of total global trade volume compared to the pre-2019 decade. This deceleration is directly attributable to intensified geopolitical risk, accelerated industrial policies (reshoring/friend-shoring), and the continued fragmentation of critical supply chains (e.g., semiconductors, rare earth minerals). This report provides corporate strategists and policymakers with definitive forecasts on regional trade balances, commodity demand, and the long-term capital reallocation necessary to ensure supply continuity.

Modeling Assumptions and Core Metrics

Our forecast utilizes a dynamic stochastic general equilibrium (DSGE) model calibrated against three primary indicators of structural change:

- Geopolitical Risk Index (GRI): Measures the probability and severity of non-market disruptions (sanctions, export bans, regional conflict). A sustained elevation in the GRI leads directly to increased redundancy investment in the model.

- Trade Restrictiveness Index (TRI): Quantifies the cumulative impact of tariffs, non-tariff barriers (NTBs), and local content requirements across major blocs (NAFTA, EU, ASEAN). TRI growth directly suppresses trade volume growth.

- Cross-Border FDI Reallocation: Tracks the shift of Foreign Direct Investment (FDI) from traditional low-cost hubs toward nearshore or domestic production centers, signaling long-term structural changes in production location.

Regional Trade Volume Forecasts (2024–2026)

The forecast shows a divergence in growth between the major blocs:

- North America (NAFTA): Imports stabilize, but the region sees significant inward FDI targeting automotive, battery, and advanced manufacturing sectors, supported by industrial policy. Exports remain constrained by continued global weakness.

- European Union (EU): Growth remains sluggish, highly dependent on energy security and the resolution of the war in Ukraine. The EU's trade strategy focuses heavily on de-risking relations with certain partners, dampening growth but increasing supply chain transparency.

- ASEAN and Emerging Asia: While still the engine of global growth, the region experiences a slowdown as capital investment is drawn toward protected domestic markets (U.S., EU). Growth becomes increasingly focused on intra-regional trade rather than exports to the West.

Policy and Corporate Strategy Mandates

The data demands a dual mandate: Secure critical inputs and manage structural cost inflation.

- Corporate Strategy: Firms must audit their supply chains for single points of failure (SPoFs) and implement a mandatory dual-sourcing policy across different geographic blocs, even if it adds 3–5% to the total unit cost. This cost is now recognized as a non-negotiable insurance premium against geopolitical volatility.

- Policy Mandate: Governments must shift subsidy programs away from CapEx (building factories) and toward R&D and Human Capital. Building a factory is easy; training the high-skilled labor force and securing the advanced IP is the real long-term competitive chokepoint. The focus must be on ensuring the skilled labor pool meets the requirements of nearshored investment.

- Reshoring vs. Diversification: The analysis shows that full reshoring is often uneconomical outside of defense-critical items. The optimal strategy is diversification across political allies (friend-shoring), requiring multinational trade and taxation treaties that specifically incentivize trade within secured partner nations.

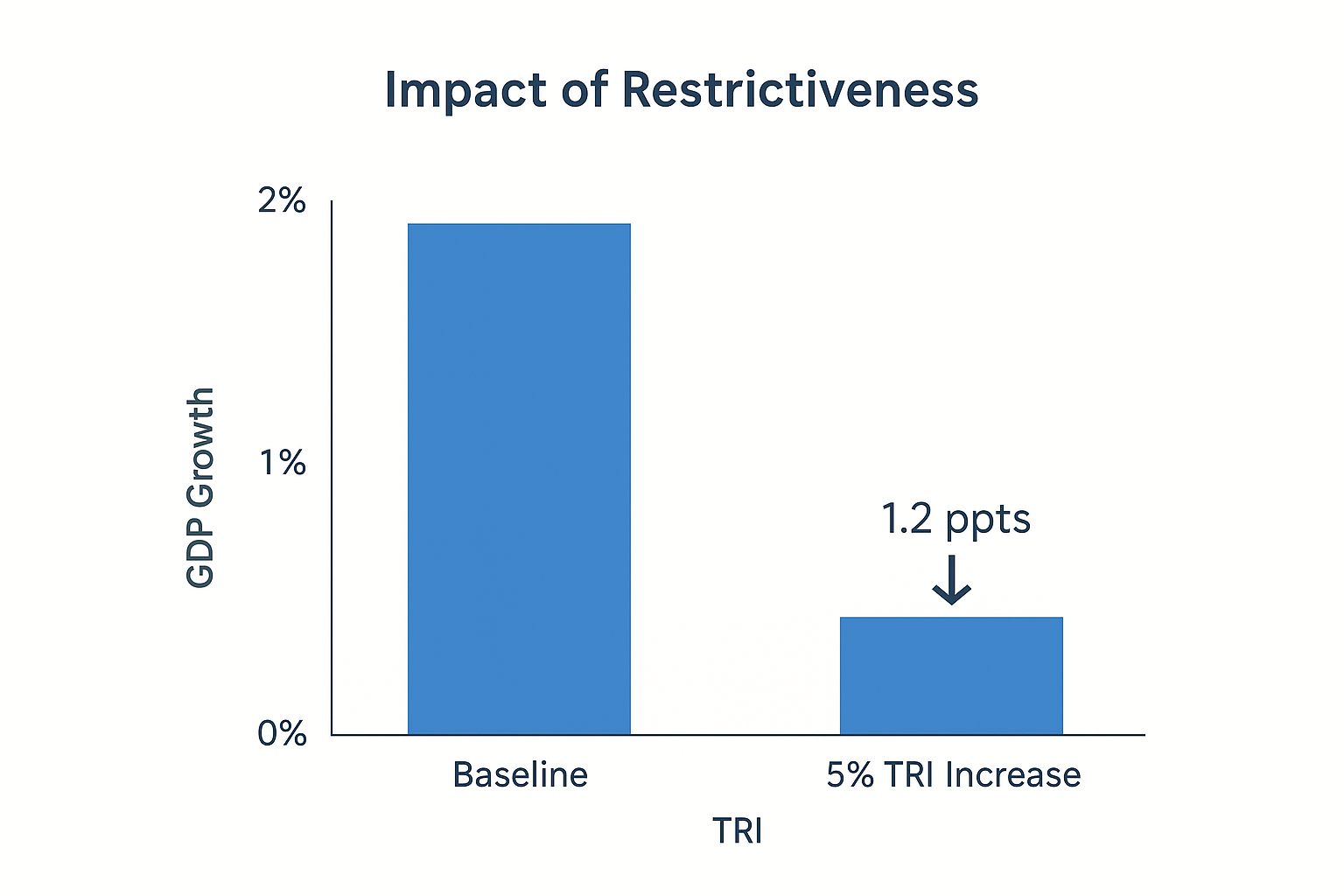

Data Visualization: Impact of Restrictiveness

Our model shows that a 5% increase in the average global Trade Restrictiveness Index (TRI) leads to a 1.2 percentage point compression in forecast global GDP growth, demonstrating the quantifiable cost of protectionism.